How home depot promo code stacking works

Many shoppers expect a single coupon to be the final step to savings. In reality, combining a home depot promo code with rebates and financing requires a specific order, eligibility checks, and a clear plan. Start by identifying which discounts are applied at checkout, which are processed after purchase as manufacturer rebates, and which savings are delivered through financing or store credit programs.

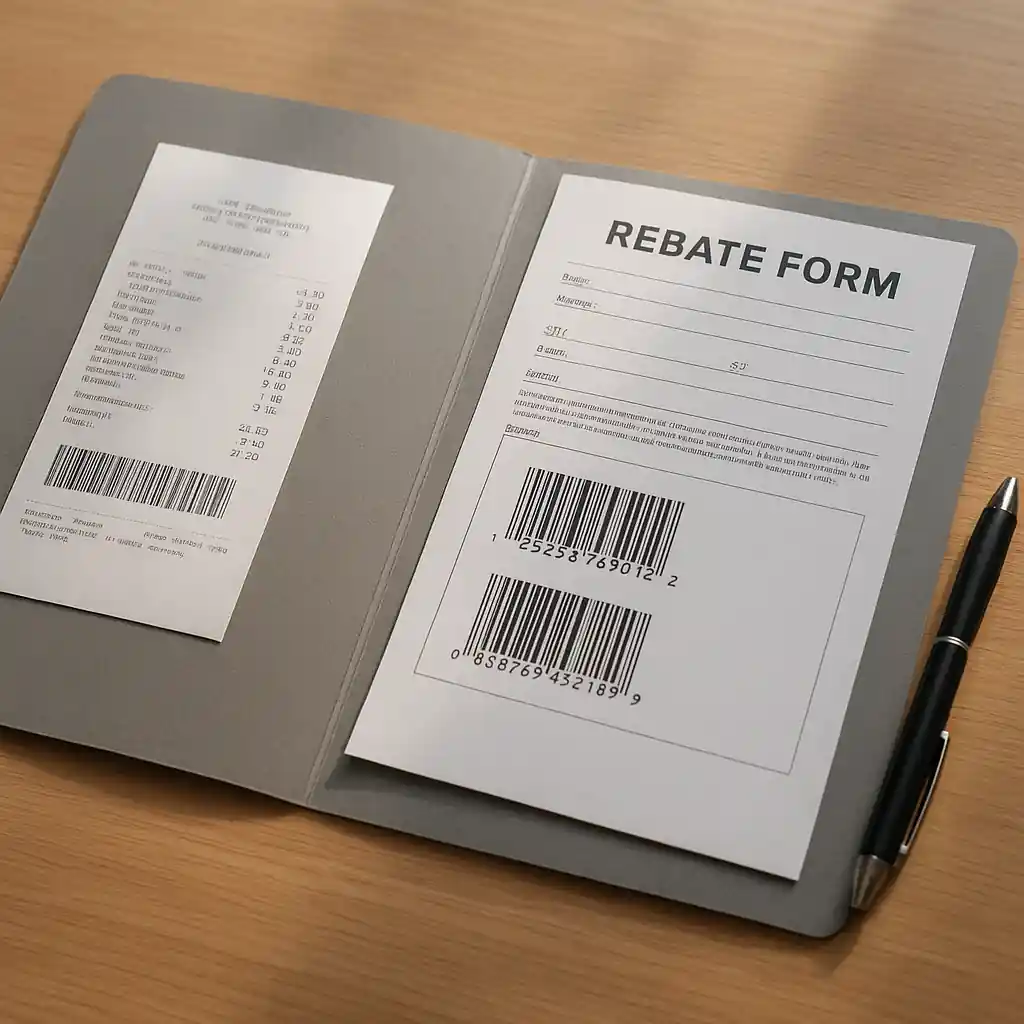

Combining home depot promo code with manufacturer rebates

Manufacturer rebates are frequently processed separately from store coupons. A typical workflow: use an eligible Home Depot promo code at checkout to reduce the sale price, then file the manufacturer rebate on the lower purchase amount when the product qualifies. Keep the rebate form, UPC, and receipt together until the rebate is paid. If the rebate requires the original receipt, do not return the item before filing.

Tip: verify rebate eligibility on the product page and read exclusions. For help filing paint and brand rebates, see the paint rebate checklist and timing advice (example resource: /stack-paint-rebates-with-home-depot-sales).

Steps to stack a coupon with a rebate

- Confirm the item is marked eligible for manufacturer rebates.

- Apply the home depot promo code at checkout to lower the taxable sales price where allowed.

- Save the receipt and product barcode/UPC for rebate submission.

- File the rebate quickly and track it until paid.

Using financing with your home depot promo code

Financing options such as Home Depot credit cards or promotional deferred-interest plans can reduce up-front cost, but rules vary. Some financing offers combine with promo codes at checkout, while deferred interest promotions often require full terms to be met. Before relying on credit, read terms at the Home Depot Credit Center (https://www.homedepot.com/c/Credit_Center) and consider guidance from consumer finance experts (https://www.consumerfinance.gov) if you are unsure about deferred-interest traps.

Practical approach: if you have an interest-free promotion, use the home depot promo code first at checkout, then choose the eligible financing to split payments. Doing so lowers your financed amount and reduces total interest risk if terms are missed.

When to choose financing vs. using cash

- Choose financing if the rate and terms are favorable and you need to preserve cash flow.

- Pay cash when short-term rebates or extra coupon stacking would be lost by using a particular credit offer.

- Check whether the financing provider allows returns without voiding the promotion.

Checkout checklist: applying a home depot promo code correctly

A short checklist at checkout prevents avoidable failures and preserves rebate eligibility.

- Confirm the promo code applies to the SKU and shipping method.

- Ensure the promo code is entered before selecting financing or gift receipts.

- Verify the final invoice shows the coupon deduction and the item price clearly for rebate submission.

- Retain all receipts, packing slips, and the product UPC for at least the rebate processing window.

If the discount fails, check coupon rules and product exclusions first. Many coupon errors come from items flagged as final sale, bundled, or ineligible categories like gas or gift cards. For general coupon troubleshooting and to find verified codes, consult the site’s comprehensive coupons overview (/home-depot-promo-code) which outlines common failure reasons and quick fixes.

Common pitfalls and how to fix them

Two common issues are stacking limits and incorrect financing selection. Stacking limits exist when Home Depot or the manufacturer restricts using a store coupon together with a rebate. Returns and cancellations can also void rebate claims if the original receipt is not available.

- Pitfall: Coupon disappears at payment. Fix: Remove non-compatible items or split the order so the eligible item can accept the promo code.

- Pitfall: Rebate rejected due to UPC mismatch. Fix: Photograph the barcode and keep the original packaging until rebate clears.

- Pitfall: Financing voids a promotion. Fix: Double-check terms on the card offer before finalizing the transaction (see /home-depot-20-off-coupon for examples of promotions that have unique terms).

Real examples and scenarios

Scenario A — Big appliance purchase: Use a verified home depot promo code to knock 5–10% off the sticker price, then choose a 0% APR financing offer to spread payments. File any manufacturer rebate after delivery using the product UPC and proof of purchase to stack savings.

Scenario B — Paint job: Buy paint during a sale, apply a Home Depot coupon at checkout to reduce the sale price, and then submit the paint manufacturer rebate for an additional return. Time your purchase during a paint sale to combine sale price, coupon, and rebate for maximum impact. Helpful reference: /stack-paint-rebates-with-home-depot-sales.

Recordkeeping best practices

- Photograph receipts and UPCs immediately and store copies in one folder or cloud drive.

- Track rebate deadlines and set calendar reminders to submit claims and follow up.

- Keep a note of which payment method you used for each purchase in case financing terms are questioned later.

Conclusion: plan your stack and protect your savings

Combining a home depot promo code with rebates and financing can significantly lower your project costs when done in the correct order. Confirm eligibility, apply coupons at checkout, document everything for rebates, and read financing terms before accepting credit. When in doubt, split large purchases or call Home Depot customer service for clarification to avoid surprises during returns or rebate processing.

Use the internal resources above for coupon rules and rebate filing examples, and keep your records organized. With a little preparation you can stack discounts safely and reduce both the sticker price and the long-term cost of big-ticket home projects.

Good luck and save smartly.